Exploring the Contextual Benefits of Environmental Reporting for Corporate Sustainability in Developing Economies: A Case Study of Zimbabwe’s Mining Sector

Thabani Ncube[1]

Martha Matashu[2]

Abstract

The paper focuses on the benefits of non-financial reporting, with an emphasis on environmental reporting in the mining companies. Thus, the purpose of this study is to investigate the context-based benefits of environmental reporting in the developing economies. This paper provide a comprehensive understanding of the contributions of environmental reporting and fosters sustainability within mining companies. A sequential exploratory research design was used to identify benefits of environmental reporting among listed mining companies in Zimbabwe. Initially, qualitative data was collected through in-depth interviews. This was followed by validation of the qualitative findings using quantitative methods. The findings show that through environmental reporting, mining companies are able to highlight their commitment to environmental stewardship, which can help to build confidence of the stakeholders. The empirical findings revealed that reporting could help companies improve the brand value, thus enhancing attractiveness of the companies to investors and various stakeholder groups. Additionally, the study established that environmental reporting in mining companies offers benefits such as enhanced transparency and accountability. It also aids in risk management by identifying and mitigating environmental risks, thereby reducing potential legal and financial liabilities. Finally, environmental reporting supports sustainability through the promotion of responsible mining, and overall, environmental reporting strengthens the reputation of the organisation and its competitive advantage in the market. In conclusion, this study revealed that understanding the benefits of environmental reporting is important for mining companies in order to foster sustainability.

Keywords: Non-financial reporting, Social licence, Investor confidence, Compliance.

Explorando os benefícios contextuais da divulgação ambiental para a sustentabilidade corporativa em economias em desenvolvimento: Um estudo de caso do setor de mineração do Zimbábue

Resumo

Este artigo analisou os benefícios da divulgação não financeira, com foco na divulgação ambiental em empresas de mineração. Assim, o objetivo deste estudo é investigar os benefícios contextuais da divulgação ambiental em economias em desenvolvimento. O trabalho fornece uma compreensão abrangente das contribuições da divulgação ambiental e promove a sustentabilidade dentro das empresas de mineração. Foi utilizado um desenho de pesquisa exploratório sequencial para identificar os benefícios da divulgação ambiental entre empresas de mineração listadas no Zimbábue. Inicialmente, foram coletados dados qualitativos por meio de entrevistas em profundidade. Em seguida, os achados qualitativos foram validados utilizando métodos quantitativos. O estudo revelou que, por meio da divulgação ambiental, as empresas de mineração conseguem destacar seu compromisso com a gestão ambiental, o que pode ajudar a fortalecer a confiança dos stakeholders. Os resultados empíricos mostraram que a divulgação pode auxiliar as empresas a melhorar o valor da marca, tornando-as mais atraentes para investidores e diversos grupos de interesse. Além disso, o estudo constatou que a divulgação ambiental nas empresas de mineração oferece benefícios como maior transparência e responsabilização. Também contribui para a gestão de riscos ao identificar e mitigar riscos ambientais, reduzindo, assim, potenciais responsabilidades legais e financeiras. Finalmente, a divulgação ambiental apoia a sustentabilidade por meio da promoção da mineração responsável e, de forma geral, fortalece a reputação da organização e sua vantagem competitiva no mercado. Em conclusão, este estudo revelou que compreender os benefícios da divulgação ambiental é fundamental para que as empresas de mineração promovam a sustentabilidade.

Palavras-chave: Relatórios não financeiros; Licença social; Confiança dos investidores; Conformidade.

1 Introduction

Environmental reporting gained momentum over the years as a non-financial reporting system that promotes sustainability in companies (Saeed, Mohammed, Kumari & Pandey, 2025; Yahaya, 2025; Pitria & Rahmawati, 2025). Contemporary literature shows that environmental reporting has positive and significant impact on the company’s equity. According to Retolaza and San-Jose, (2021) companies that practises environmental reporting stand better levels of accessing third party finance in favourable conditions. Similarly, a study by Darnall, Ji, Iwata and Arimura, (2022) assert that companies that promote sustainability through non-financial reporting realise their benefits on a long term value of the company. Ncube et al. (2025) state that environmental reporting help organisation to accrue not only financial and environmental benefits but social benefits like legitimacy. Thus, if stakeholder groups like community are protected from harm and are provided with opportunities to work their perspective of the mining activities are likely to be positive. Irrespective of these known benefits of environmental reporting, mining companies in developing economies lacks transparency and commitment on sustainability (Yahaya, 2025).

According to Saeed et al. (2025) there is need to further investigate the effects of environmental reporting on the listed companies in the sub-Saharan Africa. Moreover, Yahaya, (2025), recommends that more research should be done on the benefits of environmental reporting. It can be deduced from the two scholars that while some scholars like Mousavi, Varnamkhasti and Aghajani, (2025) focused on non-financial reporting in the Middle East countries their findings cannot be used to address challenges of environmental reporting in developing economies in Africa. Thus this paper pursues to find environmental reporting benefits that are context dependent on developing economies with a focus on Zimbabwe as a developing economy.

Conventionally, companies account for their economic position to the shareholders by providing them (the shareholders) with financial statements. Extant literature suggests that sustainability accounting and environmental reporting began in the 1960s and 1970s (Hyršlová, Becková & Kubáňková, 2015). However, Moneva, Bonilla-Priego and Ortas, (2019) argue that environmental reporting has existed for many years; it was only in the 1970s and 1980s that it took a formal shape. Moneva et al. (2019) explain that an environmental reporting system was developed in 1971 by a social audit consultancy firm ‘Abt Associates’ which provided a reporting system that was based on reporting economic figures and social and environmental impacts through a traditional balance sheet. A similar experience was carried out in Europe, although it was called Social Accounting (Retolaza & San-Jose, 2021). Moneva et al. (2019) suggest that these models did not get much acknowledgement from the business community because of the exertion in making comparisons and the low level of impact on stakeholders. According to Desai (2020), in 1972, the United Nations General Assembly decided to convene the first-ever conference on the environment called the Stockholm Conference in Sweden. The focus of the conference was on human interaction with the environment and on providing guidance to people on how to preserve and enhance environmental management. As a result, the United Nations Environment Programme (UNEP) was established to encourage United Nations (UN) agencies to integrate environmental issues into their programmes.

The development of environmental reporting ascended from anxiety about the serious ecological problems of the planet. After that, the United Nations and ecological organisations promoted environmental management (Larrinaga, Rossi, Luque-Vilchez & Núñez-Nickel, 2020). The ascendance of environmental reporting led firms that were more prone to environmental incidents, such as petrol and chemical companies, to start reporting on environmental matters or their impact on the environment (Du, Lu, Zhang & Li, 2025). Moneva et al., (2019) clarify that the environmental management systems such as ISO 14001 and EMAS, which had the aim of reflecting a public commitment to environmental aspects, were implemented later. However, there is dearth of knowledge on the significance of addressing environmental reporting in relationship to the economic, environmental and social aspects.

Table:1, below illustrates the development of environmental reporting from the 1970s, when a social balance sheet was used to disclose environmental impact and information on the aspects of interest for representatives of the organisation (Moneva et al., (2019). Fayyaz, Liu, Xu and Ramzan, (2025) assert that environmental reporting system has evolved over time to the current system, where reporting takes into account various stakeholders’ interests. Agustia, Sawarjuwono and Dianawati, (2019) acknowledges that a number of frameworks have been developed to enhance environmental reporting, mostly in developed countries with very little success stories in developing economies.

Table 1. History of environmental reporting

|

Period |

Data disclosed |

Characteristics |

|

1970s |

Social Audit (Abt) |

An analysis of the financial implications on the environment |

|

Social balance sheet (Bank of Bilbao) |

Details about topics of importance to organisation representatives |

|

|

1980s |

Social and Environmental data |

Information found in the financial statements of the company |

|

1990s |

Environmental reports |

Reports produced by putting environmental management systems into place |

|

Financial, and environmental reports |

Accounting guidelines that are relevant to environmental issues |

|

|

2000s |

Social and Environmental reports |

Reports that cover an organisation's social, economic, and environmental aspects |

|

2024 |

Social and Environmental reports |

Industry-specific reporting standards |

Source: The Authors

Myava, (2019) reveals that in 1992, the United Nations Conference on Environment and Development convened a meeting on environmental sustainability as a result of force from pressure groups and NGOs. Alaeddin, Shawtari, Salem and Altounjy, (2019) revealed that the purpose of the meeting was to focus on present and future generations' roles in promoting bases for a collaborative effort to obtain a fair balance between economic, social, and environmental needs. Christine, Yadiati, Afiah, and Fitrijanti, (2019) mention that the meeting resulted in the birth of the Rio Declaration, where numerous countries were expected to stand by the principles of sustainable development. Christine et al., (2019) explain that the laws and regulations that govern the environment were introduced. Muza, (2018) clarifies that environmental laws and regulations are meant to ensure that companies comply with environmental requirements. This implies that the Rio Declaration sought not only to introduce laws and regulations but also to ensure that companies would show compliance in their reporting.

Jere, Ndamba and Mupambireyi, (2016) mention that after the Rio Declaration, the Triple Bottom Line was developed, and the idea had a three-dimensional view of development, which included the economic, social and environmental elements. This demonstrates the requirement to reinforce the view that companies should act responsibly in line with sustainable development principles. Society requires a responsible organisation that is able to communicate its commitment to sustainable development to stakeholders (Gerged, 2021). It can be deduced that the triple bottom line emphasises the three elements, which are economic, social and environmental reporting. In short, this is how environmental reporting developed, and it is worth noting that environmental reporting is part of sustainability reporting.

2 Materials and Methods

A sequential exploratory research design was employed to identify benefits of environmental reporting among listed mining companies in Zimbabwe. The initially phase involved the collection of qualitative data using in-depth interviews with managers, professionals and technicians from Zimbabwe listed mining companies. Data saturation was achieved at 17 in-depth interviews. Subsequently, the constructs established from the qualitative phase were subjected to empirical validation through quantitative methods. In this phase, the quantitative data was collected from 400 respondents which include the technician, mine surveyor, metallurgist, geologist, safety health and environmental officer, artisan, engineer, accountant, finance manager, operations manager, CEOs, CFOs, marketing managers and human resource managers.

3 Results and Discussion

3.1 Qualitative methods

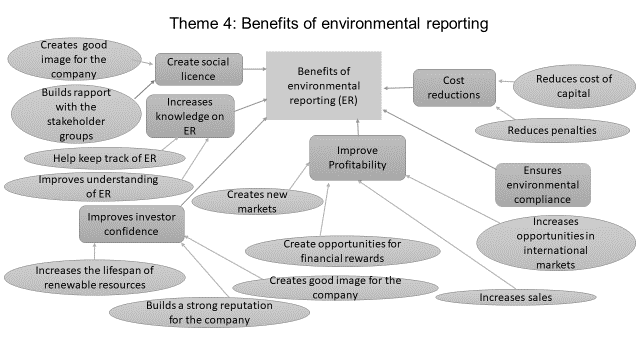

Through utilisation of qualitative methods, the study aimed to explore the benefits of environmental reporting among Zimbabwe-listed mining companies. The benefits of environmental reporting are conceptualised as long term impact or results from the implementation of environmental reporting. The results demonstrates the tangible and intangible gains accrued by companies through such reporting. The figure 1 below present the summary of emergent thematic categories.

Figure 1: Benefits of environmental reporting

Source: The Authors

A number of the participants indicated that environmental reporting leads to profitability in the medium to long-term period. This is in line with the findings of previous studies (Fuzi, et al, 2019; Fuzi, Habidin, Janudin, Yong and Ong, 2016; Jere, Ndamba and Mupambireyi, 2016; Susanto and Meiryani, 2019; Mohamed and Jamil, 2020). This was evident from their responses, as some mentioned that environmental reporting increases sales, which means an increase in revenue. P1 said, “Environmental reporting increases sales of the organisation as the supply chain system prefers to work with green economies.” Similarly, P5 had this to say: “An environmentally friendly organisation will see its return on capital increasing in the medium to the long term.” Moreover, P6; P7; P10 and P13 had the same views with P1 and P5. These perspectives reinforce Boakye et al. (2020), who found that environmental reporting improves financial performance by strengthening organisational legitimacy.

Beyond profitability, participants also indicated that environmental reporting help to penetrate international markets. Moreover, the participants revealed that when a mining company is doing well on environmental management and reporting, it is likely to get financial awards that add to the company’s income. In her own words, one participant had this to say about the benefits of environmental reporting: P4 noted: “The general improvement in environmental management and reporting can get the mining company some financial rewards from financiers or the regulators. Usually, everyone wants to work with an organisation that has improved their environmental performance, and they are ISO-14001 certified, this makes it easier to sell your products on international markets”. In consensus with P4, P15 also mentioned that being ISO 14001 helps the company to penetrate the new markets. “An organisation that monitors its environmental performance may be seen as wasting money, but, in the medium to long term, it actually helps the company to become profitable because if you are certified with ISO-14001, you have an advantage of getting into new markets.”

According to Edmans (2021), environmental management reduces risk and builds public trust in business. This is a factor that is crucial in determining whether sustainable companies enjoy a lower cost of capital. Environmental management is often taken for granted as a measure of reducing a company’s capital cost (Sidik, Yadiati, Lee & Khalid, 2019 Gonçalves, Dias & Barros, 2022; Liu, Wang & Li, 2018). Through thematic analysis, the study established that environmental reporting reduces penalties and capital costs. This means that when a company is following its environmental impacts, it is capable of effectively managing its environment and reducing the chance of being penalised for issues related to pollution. Additionally, participants mentioned that an environmentally friendly mining company attracts investors, which results in reduced capital costs. This is because the company can easily access capital when required. Participant P2 observed: “The environment will be protected because of the efforts of the mining company to manage and report their impact on the environment, and they will be kept in check on whether they are doing what they are supposed to be doing by the regulator. Secondly, it minimises the costs related to environmental management issues like penalties or fines.”

The views of P7 are in line with those of P4, P2, and P15, except for the point that environmental reporting can help the company get finances from international organisations such as the World Bank. According to P7, “The benefits of environmental reporting are that your products will be available in the global markets. And then the fact that you are reporting on environmental issues means you can easily get finances from international organisations like the World Bank. It would be easy to get money at low costs because you are actually doing environmental reporting and environmental audits.”

P8 brought another dimension or school of thought when he mentioned that environmental reporting could be viewed as costly, but he was quick to say that, in the long run, it will yield positive results. Participant P8 noted: “When it comes to cost, environmental reporting initially can be seen as costly because the mining company has to put in place measures to mitigate the impacts of their operations like dumping waste. This can be seen as time-consuming, but in the long run, it will benefit the company a great deal because investors look at the environmental reports.”

3.1.3 Create social license

In exploring the study, a significant pattern emerged that aligns with (Kathy Rao, Tilt and Lester, 2012; Patwary, Rasoolimanesh, Aziz, Ashraf, Alam and Rehman, 2025) were it was established that environmental reporting creates a social licence for the mining company to operate within the community. It was understood that informing the community through reporting makes the community feel respected and part of the company processes as they are given an opportunity to share their input. Participant P4 shared an almost similar view to one established by the GRI Annual Sustainability Report. (2022), which is that environmental reporting contributes to improved governance and stakeholder relations, enhances reputation, and builds trust with the community. “It improves the morale of the community where the mine is located. If the community gather that you are environmentally conscious, they will love the mine and become ambassadors of the mining company. They will feel respected and create a good relationship with the mining company”. P2, in support of the view by P4, had this to say: “The mining company gains trust from the community if the communities are seeing the benefits accrued from the projects of the company, they would support it, and their support delivers a social license to operate.”

3.1.4 Improves investor confidence

The study also established that environmental reporting builds confidence in investors. The participants indicated that modern investors are keen to invest in an environmentally friendly organisation. Additionally, they noted that investors prefer reputable companies and those who can manage their resources efficiently to last longer. More so, the participants indicated that a company that reports on environmental issues creates a trend analysis, allowing the investors to have a clear picture of the risk associated with the environment in the company. The findings depict those of Ning, Saeed and Kongkuah, (2025), who state that environmental reporting attracts stakeholders such as investors, customers, and employees. Participant P8 had this to say about investors’ preference: “And there are some people who, when they see that the company is not reporting on environmental issues, don’t even invest in it. So if you report, you stand a chance to get more investors because you are transparent and doing things the right way.” Similarly, P6 mentioned that investors prefer an environmentally friendly company. “The other thing is that investors prefer investing with companies that have green credentials. The green credentials attract a lot of investors because investors want to work with environmentally friendly companies”.

Miklosik and Evans, (2021) maintain that environmental reporting brings confidence to investors as information asymmetry is reduced, transparency is increased, stakeholder mobilisation is diminished, and the risk is minimised and negativity to the company. In this study, it was revealed that environmental reporting improves the company’s reputation and company sales. It boosts the morale of the employees and enhances the company’s relationships with other stakeholders. According to P10, “Environmental reporting improves the reputation of the mining company, and it also helps to improve the company sales. This is because some clients are particular about the environmental and safety issues. This also boosts the sales and the morale of the employees. When employees realise that their company is committed to environmental issues, they will feel protected and therefore boost their morale. It also helps to improve the relationship between regulatory and the mining company”.P12 noted: “It allows the reporting company and investors to conduct a trend analysis that is to follow proceedings. The other thing is that having a record will allow for the observation of changes that are happening. It also allows the comparison of what is on the ground and on documents.” P16 believes that if water is protected from pollution, it can improve its availability by at least a day. “In a country that has a scarcity of water, when you protect the water from pollution, then you would give us an extra day of resource availability. It helps to identify the problem and then helps to limit things that pollute the environment or of detriment to the environment.”

3.1.5 Ensures environmental compliance

According to Hameed et al. (2025), environmental reporting enables companies to keep track of their environmental activities as well as to maintain a compliant environmental status. Through thematic analysis, the study established that environmental reporting leads to environmental consciousness, and the company is able to track its environmental management and reporting systems. In support of Hameed et al. (2025), P7 mentioned that reporting supports the company in staying compliant with the requirements of the regulators. “When a mining company is reporting on environmental issues, it becomes compliant with local and international standards” P9 indicated that: “Environmental reporting is actually a key planning tool in terms of growth of a mining organisation because you know whether you are running a sustainable company. This will help prevent pollution and rehabilitate the environment.”

3.1.6 Improve knowledge of environmental management and reporting

The participants indicated that environmental reporting increases stakeholders' knowledge of environmental management. This is consistent with the findings of prior studies that revealed that environmental reporting increases awareness and encourages innovative ways of environmental management and reporting (Hidayat, Abbas, Lam & Sari, 2024; Hamid, Ijab, Sulaiman, Md Anwar & Norman, 2017). One participant explained that the more mining companies report on their impact on the environment, the more knowledgeable people become about the phenomenon. The participant explained that it creates awareness in the communities of pollution that is happening in their regions. Additionally, participants indicated that environmental reporting helps to protect the environment as communities are given measures of how to protect the environment.

Participant P3 argued that environmental reporting helps save the environment, create awareness and encourage innovativeness. “I think environmental reporting is critical because it helps us to save the environment; at the same time, it also helps the communities that are near the mines by creating awareness and giving alternatives on how to manage the environment on identified problems like spillage of chemicals into the river.” P1 observed: “Good environmental management boosts confidence and builds trust between the company and employees”. P2 had this to say about the benefits of environmental reporting: “Environmental reporting enforces accountability and transparency from the mining companies because they would be giving out information regarding their impact on the environment. Stakeholders will then be able to follow up on what the company is claiming to be doing. If the company has done well, its credibility and reputation will be improved.”

3.1.7 Summary of qualitative results

In analysing the benefits of environmental reporting, the study found that there were similarities between the findings of Ekins and Zenghelis, (2021) and GRI Annual Sustainability Report. (2022) with that of the study. The study established that environmental reporting reduces costs, creates a social licence for an organisation to operate, improves investor confidence, ensures consistency in compliance and improve environmental management and reporting knowledge of the different stakeholder groups. However, there was a slightly different in that this study established that the benefits of environmental reporting are context dependent.

3.1.8 Implications for the quantitative phase

The constructs identified during the qualitative phase of the study were further validated using the quantitative analysis. Key constructs included enhancing investor confidence, increasing compliance rates and attainment of a social licence to operate. Moreover, environmental reporting was found to act as a catalyst that influences profitability in the organisation by reducing costs, while simultaneously improving the awareness on environmental management and reporting practises.

3.2 Quantitative methods

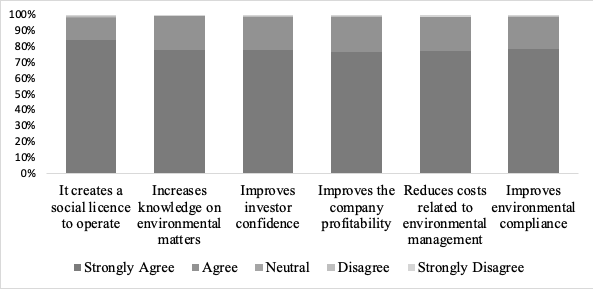

The second phase of the research served to empirically validate the findings from the initial qualitative phase of the study. The validation was conducted using quantitative data analysis, drawing on data collected from a sample of 400 respondents drawn from Zimbabwe listed mining companies. Thus, the figure 2 below illustrates the summary of the results obtained during the quantitative phase of the study.

Figure 2: Benefits of environmental reporting

Source: The Authors

Figure shows the following results: Firstly, 84% of the respondents strongly agree, and 14.3% agree that social licence is a benefit of environmental reporting. While 0.5 % were neutral, 0.3% disagreed, and 1% strongly disagreed that social licence is a benefit of environmental reporting. The majority of respondents view a social licence as a benefit of environmental reporting. Secondly, 77.8% of respondents strongly agree, and 21% agree that environmental reporting increases knowledge on environmental matters. On the other hand, 0.3% disagree, and 0.8% strongly disagree that environmental reporting helps increase understanding of environmental issues. This means that the majority of respondents acknowledge that environmental reporting can increase stakeholders' knowledge of environmental matters. Thirdly, 78% of respondents strongly agree, and 20.8% agree that environmental reporting improves investor confidence. However, 0.3% disagree, and 1% strongly disagree that environmental reporting can improve investor confidence. From the results, it can be concluded that the majority of respondents believe that environmental reporting increases the confidence level of investors.

Fourthly, a total of 76.8% strongly agree, and 22% agree that environmental reporting improves the company's profitability. On the other hand, 0.3% disagree, and 1% strongly disagree that environmental reporting does not influence the profitability of the company. Most respondents perceived that environmental reporting improves the profitability of a company. Fifthly, the study found that 77.3% strongly agree and 21.3% agree that environmental reporting reduces the costs related to environmental reporting. Nonetheless, 0.3% of respondents were neutral about the issue, while 1.3% strongly disagreed that environmental reporting leads to a reduction in costs related to environmental management. Finally, the study sought to measure the level of consensus with the view that environmental reporting improves compliance with company environmental issues. About 78.5% strongly agree, and 20.5% agree that environmental reporting improves compliance with environmental issues in the company. However, 0.3% disagree, and 1% strongly disagree that environmental reporting improves compliance within the company.

3.2.1 Summary of quantitative results

The study discerned that a comprehensive understanding of the contributions of environmental reporting facilitates the realisation of its benefits and fosters sustainability within mining companies. Through environmental reporting, mining companies are able to highlight their commitment to environmental stewardship, which can help to build trust with different stakeholders. The empirical findings revealed that reporting could help companies improve their reputation and brand value, thus making the companies more attractive to various stakeholders.

The study established that environmental reporting in mining companies offers numerous benefits, including enhanced transparency and accountability. It also aids in risk management by identifying and mitigating environmental risks, thereby reducing potential legal and financial liabilities. It also supports sustainability through the promotion of responsible mining, and overall, environmental reporting strengthens the reputation of the organisation and its competitive advantage in the market.

4 Conclusion

In conclusion, this study contributes to advancing scientific knowledge on the role of non-financial reporting, particularly environmental reporting, in the mining sector. By focusing on Zimbabwe-listed mining companies, the research provides context-specific insights into how environmental reporting enhances investor confidence, secures a social licence to operate, and raises public awareness of environmental management practices. Importantly, the findings extend existing literature by demonstrating that environmental reporting can act as a catalyst for profitability, reducing costs associated with compliance and environmental management, thereby linking sustainability practices with financial performance.

From a scientific perspective, this study differentiates itself from prior work by situating environmental reporting within the broader framework of non-financial reporting and highlighting its dual role: both as a governance mechanism and as a driver of organisational resilience. This adds nuance to the global debate on how sustainability reporting influences corporate behaviour in resource-dependent economies.

Nevertheless, the study is not without limitations. It is based on a specific national context, which may restrict the generalisability of findings to other mining jurisdictions. Furthermore, the reliance on perceived benefits rather than longitudinal performance data limits the ability to establish causal relationships between environmental reporting and profitability. These constraints underscore the need for cautious interpretation of the results.

Looking ahead, future research should explore comparative studies across different countries and sectors to assess whether the observed benefits of environmental reporting are consistent in varied institutional environments. Longitudinal analyses could also provide stronger evidence of causal links between reporting practices and financial outcomes. Additionally, examining stakeholder perceptions in greater depth particularly employees, local communities, and regulators would enrich understanding of how environmental and non-financial reporting influences organisational legitimacy and sustainability trajectories.

Overall, this study underscores the importance of environmental reporting as a strategic tool for Zimbabwe-listed mining companies, while also contributing to the broader scientific discourse on non-financial reporting and sustainability. By acknowledging both its contributions and limitations, the research provides a foundation for more robust, comparative, and longitudinal investigations into the evolving role of reporting in fostering sustainable mining practices.

5 Acknowledgments

The authors declare none financial support or any individual assistant.

6 Conflicts of Interest

The authors declares no conflict of interest in relation to this research study.

References

AGUSTIA, D., SAWARJUWONO, T., DIANAWATI, W. The mediating effect of environmental management accounting on green innovation: firm value relationship. International Journal of Energy Economics and Policy. 2019;9(2):299-306. https://doi:10.32479/ijeep.7438

ALAEDDIN, O., SHAWTARI, F. A., SALEM, M. A., ALTOUNJY, R. The effect of management accounting systems in influencing environmental uncertainty, energy efficiency and environmental performance. International Journal of Energy Economics and Policy. 2019;9(5):346-52. https://doi:10.32479/ijeep.8279

BOAKYE, D. J., TINGBANI, I., AHINFUL, G., DAMOAH, I., TAURINGANA, V. Sustainable environmental practices and financial performance: Evidence from listed small and medium‐sized enterprise in the United Kingdom. Business Strategy and the Environment. 2020 Sep;29(6):2583-602. https://doi.org/10.1002/bse.2522

CHRISTINE, D., YADIATI, W., AFIAH, N. N., FITRIJANTI, T. The relationship of environmental management accounting, environmental strategy and managerial commitment with environmental performance and economic performance. International Journal of Energy Economics and Policy. 2019;9(5):458-64. https://doi:10.32479/ijeep.8284

DARNALL, N., JI, H., IWATA, K., ARIMURA, T. H. Do ESG reporting guidelines and verifications enhance firms' information disclosure?. Corporate Social Responsibility and Environmental Management. 2022 Sep;29(5):1214-30. https://doi.org/10.1002/csr.2265

DESAI, B. H. 14. United nations environment programme (UNEP). Yearbook of International Environmental Law. 2020 Dec 1;31(1):319-25. https://doi.org/10.1093/yiel/yvab060

DU, A. M., LU, M., ZHANG, Y., LI, Z. Confucian culture and corporate environmental management: The role of innovation, financing constraints and managerial myopia. Research in International Business and Finance. 2025 Jan 1;73:102585. https://doi.org/10.1016/j.ribaf.2024.102585

EDMANS, A. Grow the pie: How great companies deliver both purpose and profit–updated and revised. Cambridge University Press; 2021 Nov 11.https://doi.org/10.1017/9781009053013

EKINS, P., ZENGHELIS, D. The costs and benefits of environmental sustainability. Sustainability Science. 2021 May;16(3):949-65. https://doi.org/10.1007/s11625-021-00910-5

FAYYAZ, A., LIU, C., XU, Y., RAMZAN, S. Effects of green human resource management, internal environmental management and developmental culture between lean six sigma and operational performance. International Journal of Lean Six Sigma. 2025 Jan 2;16(1):109-40. https://doi.org/10.1108/IJLSS-04-2023-0065

FUZI, N. M., HABIDIN, N. F., JANUDIN, S. E., ONG, S. Y. Environmental management accounting practices, environmental management system and environmental performance for the Malaysian manufacturing industry. International Journal of Business Excellence. 2019;18(1):120-36. https://doi.org/10.1504/IJBEX.2019.099452

GERGED, A. M. Factors affecting corporate environmental disclosure in emerging markets: The role of corporate governance structures. Business Strategy and the Environment. 2021 Jan;30(1):609-29. https://doi.org/10.1002/bse.2642

GONÇALVES, T.C., DIAS, J., BARROS, V. Sustainability performance and the cost of capital. International Journal of Financial Studies. 2022 Aug 5;10(3):63. https://doi.org/10.3390/ijfs10030063

GRI ANNUAL SUSTAINABILITY REPORT. Towards a global comprehensive reporting system, 2022. Retrieved from https://www.globalreporting.org/media/3yfhrjrk/gri-sustainabilityreport2022-final.pdf

HAMEED, K., SIRWAN, K., OMAR, Z. O., MOHAMMED, E. F., SOURKAN, S., SALIH, A. M., YAQUB, K. Q. Addressing the issue of poverty, economic growth, health matters, and environmental challenges. International Journal of Scientific Research in Modern Science and Technology. 2025 Mar 27;4(3):18-32. hptts://doi.org/10.59828/ijsrmst.v4i3.303

HAMID, S., IJAB, M. T., SULAIMAN, H., MD ANWAR, R., NORMAN, A. A. Social media for environmental sustainability awareness in higher education. International Journal of Sustainability in Higher Education. 2017 May 2;18(4):474-91. hptts://doi.org/10.1108/IJSHE-01-2015-0010

HIDAYAT, I., ABBAS, D. S, LAM, N. T., SARI, P. A. The role of environmental management accounting in mediating green innovation to firm value: Moderated by quality management. International Journal of Energy Economics and Policy. 2024;14(3):281-7. hptts://doi:10.32479/ijeep.15869

HYRŠLOVÁ, J., BECKOVÁ, H., KUBÁŇKOVÁ, M. Sustainability accounting: brief history and perspectives.2015. http://hdl.handle.net/10195/66997

JERE, F., NDAMBA, R., MUPAMBIREYI, P. F. Corporate reporting in Zimbabwe: An investigation of the legitimacy of corporate disclosures by major public listed companies in 2014, 2016. University of Zimbabwe Business Review

KATHY RAO, K., TILT, C. A., LESTER, L. H. Corporate governance and environmental reporting: an Australian study. Corporate Governance: The international journal of business in society. 2012 Apr 6;12(2):143-63.hptts:// doi.org/10.1108/14720701211214052

LARRINAGA, C., ROSSI, A., LUQUE-VILCHEZ, M., NÚÑEZ-NICKEL, M. Institutionalization of the contents of sustainability assurance services: A comparison between Italy and United States. Journal of Business Ethics. 2020 Apr;163(1):67-83. https://doi.org/10.1007/s10551-018-4014-z

LIU, Z., WANG, H., LI, P. The antecedents of green information system and impact on environmental performance. International Journal of Services, Economics and Management. 2018;9(2):111-24. doi.org/10.1504/IJSEM.2018.096074

MIKLOSIK, A., EVANS, N. Environmental sustainability disclosures in annual reports of mining companies listed on the Australian Stock Exchange (ASX). Heliyon. 2021 Jul 1;7(7). https://doi.org/10.1016/j.heliyon.2021.e07505

MOHAMED, R., JAMIL, C. Z., The influence of environmental management accounting practices on environmental performance in small-medium manufacturing in Malaysia. International Journal of Environment and Sustainable Development. 2020;19(4):378-92. hptts://doi.org/10.1504/IJESD.2020.110643

MONEVA, J. M., BONILLA-PRIEGO, M. J., ORTAS, E. Corporate social responsibility and organisational performance in the tourism sector. Journal of Sustainable Tourism. 2020 Jun 2;28(6):853-72.Retrieved from https://www.tandfonline.com/doi/abs/10.1080/09669582.2019.1707838

MOUSAVI SA, VARNAMKHASTI MJ, AGHAJANI M. The Role of Integrated Environmental Management Systems (IEMS) in Promoting Human Resource Sustainability in the Assaluyeh Oil Field. International Journal of Mathematical Modelling & Computations. 2025 Jun 10;15(3):181-97.hptts:// doi.org/10.71932/ijm.2025.1207725

MUZA, C. An assessment of the relevance of Environmental Management Accounting for sustainability in Zimbabwe’s extractive industries. (Doctoral dissertation, Stellenbosch: Stellenbosch University); 2018

MYAVA, J. E. Development of an environmental reporting framework for the industrial sector in Tanzania. University of South Africa (South Africa); 2019

NCUBE T, MUSVOTO W S, MATASHU M. Factors influencing corporate environmental reporting amongst mining companies in developing countries. International Journal of Business Ecosystem & Strategy (2687-2293). 2025 Dec 11;7(5):22-30. https://doi.org/10.36096/ijbes.v7i5.957

NING, W., SAEED, U. F., KONGKUAH, M. Saving the environment in emerging markets: The synergistic roles of corporate ownership structure, financing strategy, and innovation capacity. Business Strategy and the Environment. 2025 May;34(4):5114-38. https://doi.org/10.1002/bse.4245

PATWARY, A. K., RASOOLIMANESH, S. M., AZIZ. R. C., ASHRAF, M. U., ALAM, M. M., REHMAN, S. U. Assessing environmental performance through environmental management initiatives, green extrinsic and intrinsic motivation, and resource commitment in Malaysian hotels. International Journal of Hospitality & Tourism Administration. 2025 Mar 15;26(2):311-42. hptts://doi.org/10.1080/15256480.2024.2312474

RAIMO, N., CARAGNANO, A., ZITO, M., VITOLLA, F., MARIANI, M. Extending the benefits of ESG disclosure: The effect on the cost of debt financing. Corporate Social Responsibility and Environmental Management. 2021 Jul;28(4):1412-21. https://doi.org/10.1002/csr.2134

RETOLAZA, J. L., SAN-JOSE, L. Understanding social accounting based on evidence, 2021. Retrieved from https://journals.sagepub.com/doi/10.1177/21582440211003865?icid=int.sjabstract.citing-articles.83

SAEED, M. M., MOHAMMED, S. S., KUMARI, M., PANDEY, G. The impact of corporate environmental reporting on the financial performance of listed manufacturing firms in Ghana (Csr‐24‐2036). Corporate Social Responsibility and Environmental Management. 2025 Jan;32(1):1230-44. hptts://DOI: 10.1002/csr.3015

SIDIK, M. H., YADIATI, W., LEE, H., KHALID, N. The dynamic association of energy, environmental management accounting and green intellectual capital with corporate environmental performance and competitive. International Journal of Energy Economics and Policy. 2019;9(5):379-86.https://doi.org/10.32479/ijeep.8283

SOMJAI, S., FONGTANAKIT, R., LAOSILLAPACHAROEN, K. Impact of environmental commitment, environmental management accounting and green innovation on firm performance: An empirical investigation. International Journal of Energy Economics and Policy. 2020;10(3):204-10. doi:10.32479/ijeep.9174

SUSANTO, A., MEIRYANI, M. Antecedents of environmental management accounting and environmental performance: Evidence from Indonesian small and medium enterprises. International Journal of Energy Economics and Policy. 2019;9(6):401-7. doi:10.32479/ijeep.8366

YAHAYA, P. D. Institutional ownership and environmental reporting. Available at SSRN 5130854. 2025 Feb 10. https://dx.doi.org/10.2139/ssrn.5130854